EU Intends to Engage in Trade War with China Amid Chinese Cars Nearing 10% of Monthly Sales in Europe

06/08 2026

06/08 2026

347

347

"Describing Trade and Investment Relations with China as 'Unsustainable'" Compiled by | Yang Yuke Edited by | Li Guozheng Produced by | Bangning Studio (gbngzs)

The EU and China are on the brink of a full-blown trade war.

The good news is that on June 3, the European Commission confirmed that EU Trade Commissioner Maroš Šefovič would meet with Chinese trade representative Li Chenggang on June 4 during the OECD Ministerial Council Meeting in Paris, France, leaving room for alleviate (Note: ' alleviate ' is kept as pinyin here since it's a term being defined in context; in a full translation, it would be replaced with 'easing' or 'de-escalation').

A few days ago, on May 29, the European Commission quietly held a closed-door meeting on "China issues" in Brussels, Belgium. Afterward, the EU issued a statement claiming that trade and investment relations with China were "unsustainable," warning EU citizens and businesses, and considering new restrictive measures against China, not ruling out the possibility of a trade war.

Subsequently, Chinese Foreign Ministry spokesperson Mao Ning responded, stating that whether it's "de-risking and reducing dependence" or the so-called "trade balance," they are essentially protectionism.

China-EU trade tensions have suddenly escalated.

In recent months, the EU has been seeking to combat alleged "Chinese overcapacity" and address its record €359 billion trade deficit with China.

Earlier this year, the EU unveiled the Industrial Accelerator Act and the Cybersecurity Law, attempting to exclude Chinese companies from the EU market. China has vowed to retaliate.

According to the EU's plan, national leaders will propose assessment recommendations at the June 18 summit to authorize the European Commission to propose new trade initiatives. However, a major issue facing the EU is the difficulty for member states to reach a common stance.

Countries like France are pushing for tougher measures against China, while export-dependent nations like Germany do not want to confront Beijing. Germany has long relied on exports accounting for roughly 40-50% of its GDP, with exports to China nearing 20%.

Soumaya Keynes, economics columnist for the Financial Times, questioned whether tariffs might buy time but would not address Europe's fundamental weaknesses.

The crux of the issue lies in whether Europe will use this time to reform: reducing structural rigidities, enhancing competitiveness, and adopting more strategic actions.

However, recent developments inspire little confidence. Although the EU's "China threat" narrative has persisted for three years, little progress has been made in establishing alternative supply chains in critical areas such as semiconductors and key minerals.

According to Chinese official data, in 2025, the EU was China's second-largest export market; as of 2026, exports to the EU have grown by 19% year-on-year.

Bloomberg Economics estimates that a one-year disruption in China's supply of rare earths and permanent magnets could pose around $4.4 trillion in risks to global GDP. If supplies were cut off, production lines in many industries would gradually grind to a halt.

▍01 Europe: No Alternative

EU commissioners refer to the threat from China as "China Shock 2.0." They accuse China of exporting overcapacity and disrupting other countries' markets.

China denies this accusation.

In 2025, the EU's goods trade deficit with China widened to €359 billion ($418 billion), up nearly 15% from a year earlier and more than double the deficit in 2019 (pre-pandemic).

According to Chinese official data, in 2025, China sold nearly €560 billion worth of goods to the EU, making it China's second-largest export market. In 2026, China continued its trend of significant growth, with exports to the EU rising 19% year-on-year so far, compared to 8% growth in 2025.

According to market research firm Dataforce, in April this year, Chinese automakers achieved a record 9.8% monthly market share in Europe (covering the EU, UK, and EFTA markets). Compared to April 2025, sales by Chinese automakers surged 114% to 112,992 units.

Among them, SAIC MG grew 38%, leading with 30,066 units sold; BYD increased 124% to 28,186 units; and Chery jumped 344% to 25,656 units. These three automakers accounted for three-quarters of Chinese sales in Europe. During the same period, electric vehicle sales grew 111% to 38,281 units, while plug-in hybrid vehicle sales soared 256% to 34,503 units.

From January to April, MG led with 110,413 units sold, followed by BYD with 102,068 units and Chery with 95,564 units.

In the UK, Chery's market share rapidly rose after entering the market in 2024. According to Dataforce, Chery held a 6% market share from January to April 2026, surpassing Ford, Toyota, and Nissan. The Jetour 7 became the best-selling model in the UK in March.

Overall, a recent report by Rhodium Group stated that Chinese foreign direct investment (FDI) in Europe (defined as the EU and UK) grew 67% in 2025 to €16.8 billion ($19.6 billion), reaching a seven-year high.

China is also making "nearshoring" investments in countries close to the EU, such as Morocco, which have free trade agreements with the EU and could provide a pathway for future EU tariffs. European senior officials have called this a "very, very serious issue."

Meanwhile, European exports to China continue to weaken. In 2025, European exports to China fell to just under €200 billion.

The countermeasures under discussion include tariffs, quotas, and "safeguard measures" that would force European companies to diversify their supply chains, reduce reliance on Chinese manufacturers, and decrease dependence on China as a major supplier of strategic industrial minerals.

A commentary in China Daily stated that the real problems faced by European companies are not caused by China but by high energy costs, heavy regulations, expensive compliance requirements, and layers of new rules in environmental, digital, and competition areas.

▍02 Over-reliance on Supply Chains

Last year, European factory managers repeatedly called government officials with an urgent message: "We have only a few days' supply left." At the time, China restricted exports of rare earth materials, essential for manufacturing electric vehicle engines, wind turbines, defense equipment, and semiconductors. Factories were days away from halting production.

De-risking transformed from Brussels jargon into a factory floor emergency. Andrew Small, a transatlantic fellow at the German Marshall Fund, stated, "It's clear that China is no longer a reliable supplier to Europe. Chinese decisions could lead to the closure of significant European industries."

The hardest-hit sectors include the industrial economy, such as electric vehicles, batteries, solar panels, wind turbines, defense, pharmaceuticals, semiconductors, and robotics.

The vulnerabilities are more severe than most realize, not at the finished product level but at the component and refining stages. For Europe, rare earth processing, battery-grade chemicals, pharmaceutical precursors, and legacy chips represent bottlenecks where China holds near-total dominance.

The list continues to grow. Small warned, "The more industrialized Europe becomes, the more industries it has that rely on Chinese inputs." If the chemical industry contracts under pressure from cheap Chinese imports, manufacturers in dozens of European industries will lose another domestic input. Dependence breeds more dependence.

Europe finally realizes it chose efficiency over resilience, and China has quietly established control over critical industrial bottlenecks.

"This is a long-term Chinese strategy," said Andrew Small, director of the Asia program at the European Council on Foreign Relations. "China is taking its time, and any other attempts to establish alternative supply sources will be suppressed."

By influencing availability, pricing, and supply, China can "weaponize" trade, leaving the EU vulnerable to supply disruptions, price shocks, and export restrictions.

A 2024 European Commission study revealed that among 204 commodities the EU depends on, 64 come from China, accounting for one-third. According to the European Commission, China now supplies 98% of Europe's solar panels, 54.4% of its machinery and vehicles, and 9.8% of its chemicals.

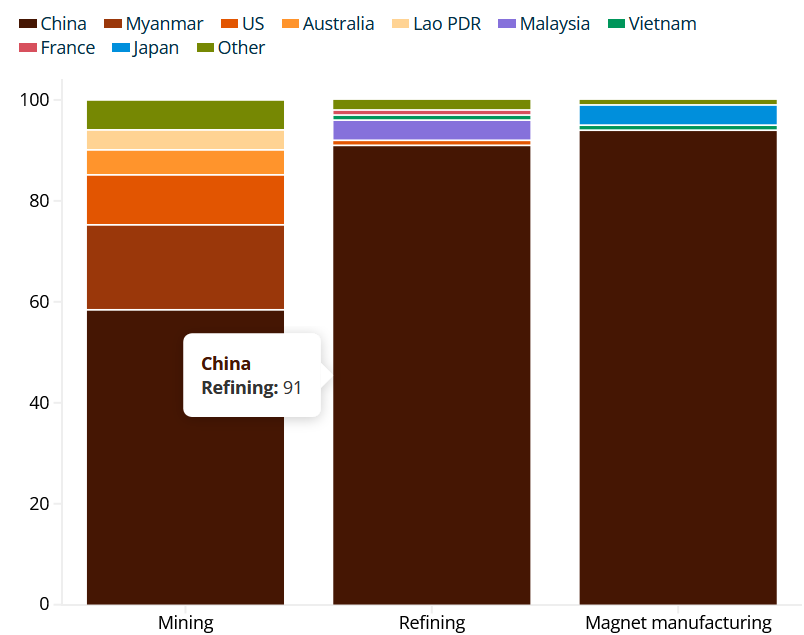

Europe's over-reliance extends beyond finished products. China wields significant influence in the middle stages of supply chains—production, refining, and processing—for raw materials and critical components.

Currently, the EU imports 97% of its magnesium for next-generation batteries and aluminum alloys; 100% of its rare earths for permanent magnets are refined in China.

Sixty to seventy percent of the world's lithium is processed in China. According to the International Energy Agency, China controls 86% of global polysilicon production and is expected to reach 88% by 2030, making it even harder for the EU to establish a fully indigenous solar industry.

EU industrial chief Stephane Sejourne warned last month that EU companies are not doing enough to reduce severe dependence on China, with few European firms factoring in geopolitical and supply chain risks.

Sejourne also stated in media comments that the EU should increase its use of trade defense measures like import quotas and tariffs to protect companies from Chinese imports.

▍03 De-risking, Not Decoupling

On May 29, the European Commission emphasized its plan to reduce risks from China rather than decouple. Europe hopes to maintain trade relations with China while reducing risk exposure in areas like raw materials, batteries, chips, solar, and other strategic supply chains.

While full autonomy may be difficult to achieve, the goal should be to prevent economic efficiency from becoming a security issue. Alicia Garcia Herrero, an adjunct professor at the Hong Kong University of Science and Technology, stated, "This occurs when dependence on a single supplier creates leverage for geopolitical coercion in critical areas like supply chains, raw materials, or technology."

Jacob Gunter, head of the "Economy and Industry" program at the Mercator Institute for China Studies, said Europe possesses the technology to build its own capabilities and is even prepared for significant capital expenditures to reduce risks. "It's not a question of whether we have the money to do this but whether we have the political will. I don't think we do yet," he said.

Herrero emphasized that Europe lacks the infrastructure and skills to replicate China's manufacturing ecosystem or rare earth processing in a short time. However, she explained, "Dependencies that can realistically be reduced within the next five years include partial diversification of components and critical inputs through new procurement rules."

The key lies in whether the EU's de-risking plans are robust enough and whether member states cooperate. "I don't think most European leaders have truly considered all these dependency risks seriously. I think they're all focused on the short term... So, in that sense, I do worry about the credibility of the de-risking agenda," Herrero added.

There is also a deeper dilemma. European companies are increasingly caught between Brussels and Beijing. The EU urges companies to distance themselves from China, while Beijing may respond with export controls, market restrictions, or subtle pressure on European companies in China.

German automakers, the hardest hit, must choose: align with EU policies and risk losing a key growth market or protect revenue from China and face domestic political scrutiny.

Small said, "Economically, continuing this cycle no longer makes sense." Europe seeks economic security rather than provoking a full-blown confrontation with China, and Beijing is aware of this.

(This article partially synthesizes reports from Automotive News, Bloomberg, Euro News, and the Financial Times, with some images sourced from the internet.)

-

![]()

When European Factories Face Idle Capacity, Chinese Brands Offer a ‘Traditional Chinese Remedy’

-

![]()

SEER Robotics Passes IPO Hearing: How Valuable Is the 'First Robot Brain Stock?'

-

![]()

5 Years, 170 Billion Yuan Wealth Vanishes: Where Did Wei Jianjun Go Wrong?

-

![]()

What Exactly Has Changed with the AI That Automatically Opens a Browser to Search Xiaohongshu?

-

![]()

Over 3,000 Heat-Related Deaths Daily, Yet India Imposes Ban on Chinese Air Conditioner Imports: Unraveling the Underlying Motives

-

![]()

Second-Hand Car Prices Plummet: Are Gasoline Vehicles on the Verge of Collapse?

-

![]()

800V vs. 48V: Which Reigns Supreme? Online Clash Between Executives Intensifies Debate Over Li Auto and NIO's Suspension Systems | MIRROR Pro

-

![]()

Anthropic Files, MiniMax Rushes for A-Share Listing, but What I Really Want to Discuss is the M3 Model