Li Auto Faces Triple Challenges: Can Li Xiang Steer Clear of the 'Backpedaling' Crisis?

07/03 2026

07/03 2026

557

557

Unveiling Business Essence, Delving into Corporate Core

Author | Yang Cheng

As major automakers recently unveiled their June performance reports, Li Auto (02015.HK, NASDAQ:LI), once a frontrunner in the rankings, appeared notably lackluster in this round of delivery comparisons. With a mere 30,895 units delivered in a single month, the company experienced a year-on-year decline of 14.84%. Extending the analysis to the first half of the year, Li Auto's cumulative deliveries of 193,500 units marked a 5.1% year-on-year decrease, making it the sole NEV manufacturer among the leading new forces to suffer negative growth.

This set of underwhelming data undoubtedly casts a shadow over Li Auto's annual performance assessment. Chairman Li Xiang had ambitiously set a target to achieve a year-on-year sales increase exceeding 20% by 2026, with a full-year goal of 487,600 units. However, as of mid-year, the completion rate for this target stands at less than 40%.

To meet its lofty target, Li Auto must elevate its average monthly deliveries to 49,000 units in the remaining half of the year. Notably, this figure significantly surpasses its average monthly deliveries of 32,200 units in the first half of the year.

01 The Fall from Grace of the Former Sales Champion

On July 1, various NEV manufacturers released their June sales performance reports. While some surged ahead, others, once at the pinnacle of sales, found themselves trailing.

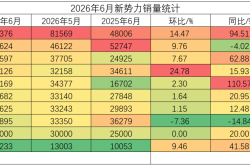

In terms of June sales, Leapmotor led the pack with 93,376 monthly deliveries, a year-on-year surge of 95%, and cumulative deliveries of 356,500 units in the first half of the year, up 60.8% year-on-year. HiMo delivered 50,624 units, with cumulative deliveries of approximately 240,000 units in the first half of the year, marking an 18.6% year-on-year increase. NIO and XPENG delivered 40,597 and 40,126 units, respectively, both surpassing the 40,000-unit mark. In stark contrast, Li Auto, once the sales champion among new forces, appeared somewhat lackluster.

In June 2026, Li Auto delivered 30,895 new vehicles, a year-on-year decline of 14.84%, failing to reach the 40,000-unit milestone and widening the gap with other leading new forces. In the first half of 2026, Li Auto's cumulative deliveries were approximately 193,500 units, a year-on-year decrease of 5.1%, making it the only NEV manufacturer among the leading new forces to experience a year-on-year decline in cumulative sales.

However, as recently as March this year, Li Xiang, Chairman and CEO of Li Auto, publicly declared that the company's sales target for 2026 was a year-on-year increase of over 20%, corresponding to full-year sales exceeding 487,600 units. Based on the current progress, this target faces significant hurdles. Calculating based on the full-year target of 487,600 units, as of the end of June, Li Auto had only completed 193,500 deliveries, with a target completion rate of approximately 39.68%. This implies that Li Auto needs to achieve approximately 294,100 sales in the second half of the year, requiring average monthly deliveries of over 49,000 units in the remaining six months to meet the set target.

For comparison, Li Auto's average monthly deliveries in the first half of this year were only about 32,200 units. Even in March, its best-performing month, deliveries were only 41,100 units, still about 8,000 units short of the average monthly level required to meet the full-year target. The underwhelming delivery data in the first half of the year is inexorably increasing the risk of Li Xiang 'backpedaling' on his promises.

To meet the 20% growth target, Li Auto must not only swiftly reverse the year-on-year decline in the second half of the year but also continuously break its own sales records for several months.

02 Organizational Restructuring Amid Performance Pressure

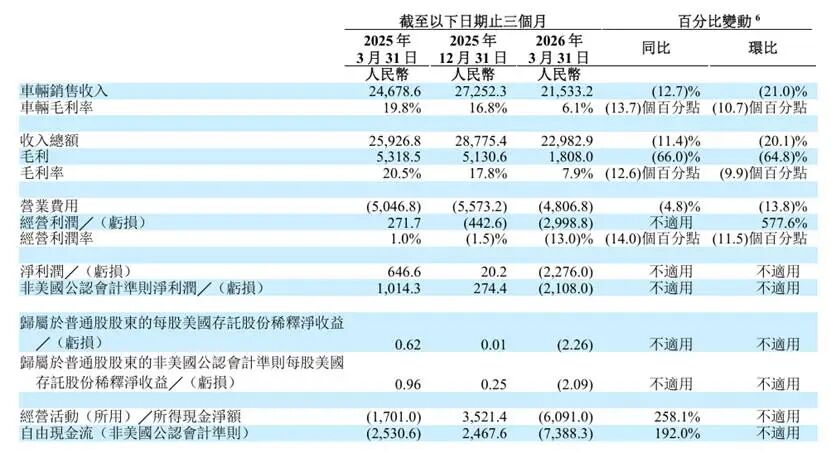

Corresponding to the sales pressure, Li Auto's performance in the first quarter of 2026 also failed to impress. Financial reports revealed that the company achieved revenue of RMB 22.983 billion in the first quarter, a year-on-year decrease of 11.4%; net profit loss was RMB 2.290 billion, compared to a net profit of approximately RMB 650 million in the same period last year, marking a turn from profit to loss.

The shift from 'profit generation' to 'loss generation' is attributed to a significant compression of gross profit margins. In the first quarter, Li Auto's overall gross profit margin plummeted from 20.5% in the same period last year to 7.9%, a drop of 12.6 percentage points; the vehicle gross profit margin, representing the profitability of the core car-making business, fell from 19.8% to 6.1%. The pressure of performance decline is compelling Li Auto to undertake internal reforms.

Recently, media reports indicated that Li Auto is set to undergo a new round of organizational restructuring centered on the product decision-making process, planning to split some key functions of the product department and integrate them into the research and development (R&D) department. Specifically, the electric vehicle definition team and the autonomous driving end-product team will be integrated into the vehicle R&D and base model R&D camps, respectively.

This means that the 'three-tier circulation' decision-making chain, formerly composed of the product line, product department, and R&D department, will achieve direct dialogue between the product line and R&D department by extracting the functions of the product department. The core essence of this power consolidation, which returns product definition to R&D, is to minimize internal tug-of-war cycles and enhance the efficiency and quality of intelligence and hardware implementation.

It is worth mentioning that this is a continuation of Li Auto's multiple organizational restructurings this year. From reorganizing the R&D system into three teams—base model, software ontology, and hardware ontology—at the beginning of the year to further streamlining decision-making levels now, Li Xiang's frequent organizational refactorings are essentially addressing past 'system bloat.'

As of the close of trading on July 1, 2026, Li Auto's Hong Kong stock was priced at HKD 46.08 per share, having cumulatively fallen by approximately 37.7% since the beginning of the year, with a total market value shrinking by over HKD 40 billion compared to the start of the year. Under the triple pressure of sales, profitability, and organizational efficiency, Li Xiang has little time left to meet his targets.

END

The images in this article are sourced from the internet.

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma