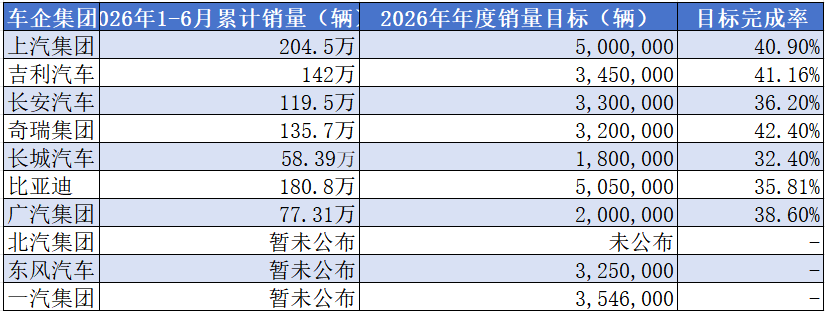

Year's First-Half Target Achievement Rates of Seven Leading Auto Groups: Highest at 42.4%, Lowest at 32.4%, All Buoyed by Exports

07/03 2026

07/03 2026

558

558

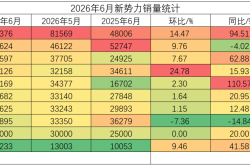

As of the evening of July 2, among the major automotive conglomerates, only Dongfeng, FAW, and BAIC had yet to disclose their June sales figures. The remaining automakers, including SAIC Group, BYD, Geely Automobile, Changan Automobile, Chery Automobile, Great Wall Motor, and GAC Group, have all released their sales results. In terms of target achievement rates, two distinct tiers emerge, delineated by 40% and 30% benchmarks. Geely, SAIC, and Chery surpass the 40% mark, while Changan, BYD, and Great Wall Motor exceed 30%.

Chery currently leads the pack with the highest target achievement rate at 42.4%. In the first half of the year, Chery sold 1.357 million vehicles, aiming for an annual target of 3.2 million. Chery's primary growth driver in the first half was exports, with a cumulative total of 943,817 vehicles exported, marking a 71.5% year-on-year increase and setting a new record for Chinese automobile exports exceeding 900,000 vehicles in a half-year period. Notably, June alone saw exports surpass 190,000 vehicles, another record. The new energy sector also witnessed rapid growth, with Chery selling 475,238 new energy vehicles in the first half, a 32.3% year-on-year increase; sales exceeded 100,000 vehicles for three consecutive months, and wholesale volume ranked among the top three in the industry.

However, Chery's overall performance in the domestic market appears somewhat lackluster, with the focus now shifting towards enhancing domestic sales.

Geely ranks second in terms of target achievement. This is not surprising, given that Geely has already revised its annual target upwards in the first half of the year. Geely sold 1.42 million vehicles in the first half, targeting 3.45 million annually, with a target achievement rate of 41.16%. Geely has not only experienced sales growth but also a significant improvement in its internal sales structure, characterized by a surge in high-end vehicle sales and overseas market expansion. From January to June, overseas export sales reached 474,228 vehicles, a 158% year-on-year increase, surpassing the total export sales for the entire year of 2025. Sales of the high-end brand Zeekr reached 178,370 vehicles in the first half, a 97% year-on-year increase, contributing to Geely's strong performance.

Geely appears to be the most well-adjusted among the major automakers, with its product structure, brand portfolio, and costs all exhibiting renewed vitality post-reforms.

Third on the list is SAIC, which sold 2.045 million vehicles from January to June, making it the only automaker in the industry to exceed 2 million vehicles in half-year sales, with an annual target of 5 million. SAIC's sales are bolstered by independent brands and exports. Official data shows that from January to June, SAIC's independent brands sold a cumulative total of 1.469 million vehicles, a 12.6% year-on-year increase, accounting for 71.8% of the group's sales. In overseas markets, SAIC sold a cumulative total of 735,000 vehicles, a significant 48.7% year-on-year increase, ranking among the top in the industry. SAIC Group is experiencing growth across multiple areas this year, with Shangjie and SAIC Passenger Vehicles witnessing rapid growth.

SAIC's next focus is on its joint venture segment. If the joint venture segment can maintain stable output, SAIC will solidify its top position. Moreover, given the industry's tendency to perform better in the second half of the year, SAIC's sales volume in the second half of the year is expected to significantly exceed 2 million vehicles, potentially returning to a scale of 5 million vehicles.

The target achievement rates above 30% are, in order, GAC Group, Changan Automobile, BYD, and Great Wall Motor. GAC Group has a target achievement rate of 38.6%. The group's total vehicle sales were 773,100 units, a 2.35% year-on-year increase, with energy-saving and new energy vehicles accounting for 62.82% of sales. Exports of independent brands maintained a doubling growth rate, reaching a cumulative total of 121,500 units in the first half, a 132% year-on-year increase, nearing the level of the entire previous year. In terms of sales structure, sales of independent brands were 345,952 units, a 35.69% year-on-year increase. In GAC's independent segment, the Qijing, a collaboration with Huawei, was launched in June and is expected to become a growth point in the second half of the year.

Currently, GAC faces pressure as its joint venture segment experiences a decline. Additionally, the reform dividends of Aion and Hyper have yet to be fully realized.

Changan Automobile delivered a total of 1,195,600 new vehicles in the first half of 2026, including 402,000 overseas deliveries, a 35.1% year-on-year increase, and 456,000 new energy deliveries, a 5.2% year-on-year increase. Changan Automobile's target sales volume for 2026 is 3.3 million vehicles, with a target achievement rate of 36.2%. The core incremental growth comes from Qiyuan, which delivered a cumulative total of 173,822 vehicles in the first half, a 102.6% year-on-year increase, with the Qiyuan Q05 being the main sales contributor. Secondly, Shenlan Automobile delivered a cumulative total of 164,156 vehicles, a 14.6% year-on-year increase. Avatr delivered 7,459 vehicles. As the main brand, Changan delivered 329,800 vehicles, and Changan Kaicheng delivered 117,200 vehicles.

Changan's characteristic is balance, with its fuel vehicles stabilizing the foundation, while overseas markets, new energy, and commercial vehicles all contribute, showing overall resilience. However, Avatr's progress in premiumization is slow, and Shenlan, as the core contributor, has stagnant monthly sales.

BYD has a target achievement rate of 35.81%. BYD's cumulative sales in the first half of this year exceeded 1.808 million vehicles, with an annual target of 5.05 million vehicles. However, battery supply seems to be constraining BYD's sales growth. Previously, BYD Chairman Wang Chuanfu stated that sales are expected to gradually increase from the second half of the year, with an increase of 20,000 to 30,000 vehicles per month until the end of this year. If this calculation holds, BYD's monthly sales are guaranteed to increase to 520,000 vehicles by December this year, setting a new record for monthly sales. Secondly, exports: Wang Chuanfu judges that BYD will exceed its target of 1.6 million vehicles in overseas markets this year. These two points can ensure that BYD achieves its annual target this year.

Great Wall Motor has a target achievement rate of 32.4%. Sales in June were 108,100 units, compared to 110,700 units in the same period last year, a 2.36% year-on-year decrease. Great Wall's cumulative sales this year are 583,900 units, a 2.48% year-on-year increase. Great Wall's core sales growth has now shifted to overseas markets, with overseas sales in June reaching 60,168 units, accounting for more than 50% of the sales structure in June. Great Wall's cumulative overseas sales from January to June were 291,400 units, also accounting for more than 50%. Great Wall's current sales volume is around 100,000 units, the lowest among the major independent automaker groups. Great Wall is currently adjusting its brand structure, seemingly prioritizing brand upward mobility over sales volume.

In summary, overseas sales have emerged as a key growth factor for the seven major independent automakers in the first half of this year. This trend is linked to the current contraction of the Chinese automobile market. Data from the China Passenger Car Association shows that from June 1-21 this year, retail sales in the national passenger car market were 913,000 units, a 23% year-on-year decrease compared to the same period in June, and a 7% month-on-month increase; cumulative retail sales since the beginning of the year were 8.012 million units, a 20% year-on-year decrease. Against this backdrop, it is remarkable that several automaker groups have maintained positive growth.

Secondly, among the aforementioned major groups, only BYD and Great Wall do not have joint venture segments, while the joint venture segments of the remaining automakers are facing significant pressure. Currently, joint ventures are primarily focused on fuel vehicles and are still in the early stages in the new energy sector. Some excellent products have begun to show promising market performance, such as the Buick Electra E7 from SAIC-GM, the ID.9 X from SAIC Volkswagen, and the Bo Zhi (bZ4X) series from GAC Toyota. Whether the joint venture segments can rise will be crucial for automaker groups to break through.

Third, due to the sharp contraction of the fuel vehicle segment in the first half of the year, automakers focused on fuel vehicles have not performed well in the domestic market. This has also compelled automakers to increase resource investment in the new energy segment. However, fuel vehicles have relatively good sales in overseas markets, creating a somewhat contradictory situation.

In terms of target achievement rates, SAIC and BYD will continue to vie for the top spot in the industry this year, and both automakers may simultaneously surpass the 5 million unit mark. The third place in the industry will likely go to Geely, which has strong development momentum this year. Chery and Changan will compete for fourth place, with both automakers having their strengths, and the competition is expected to be fierce. However, from the perspective of the industry's sales distribution pattern, the sales scale of the top five independent brands is continuously expanding, while Great Wall, in sixth place, is comprehensively enhancing its high-end products and overseas market share, showing an increasingly concentrated effect overall.

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma