‘Mid-Term Exam’ Results for New Energy Vehicle Startups: Some Lead, Others Lag

07/03 2026

07/03 2026

518

518

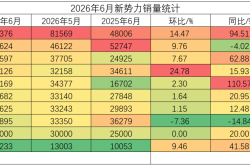

On July 1, several new energy vehicle (NEV) startups unveiled their delivery figures for June. As anticipated, Leapmotor retained its top spot among the newcomers, this time extending its lead over the runner-up by over 50,000 units—a substantial margin that is by no means an overstatement. NIO and XPENG both rebounded to the 40,000-unit mark, each showing steady progress. Only Li Auto experienced a 14.84% decline both year-over-year and month-over-month, slipping from its usual leading position to fourth place.

While these numbers may appear impersonal, they reveal vastly different survival scenarios for each company. Some have found new growth avenues through overseas expansion, others are gradually recovering with a multi-brand strategy, and some are stuck in a rut of product iteration, trapped in a stagnant situation. Halfway through the year, the competitive landscape among these new forces has undergone a significant transformation compared to the start.

Leadership Shuffle at the Top

Leapmotor delivered 93,376 vehicles globally in June, marking a 94.51% year-over-year increase and setting another brand record for monthly deliveries. With 356,487 units delivered in the first half of the year, it leads NIO, the second-place contender, by over 160,000 units, significantly widening its advantage. In addition to its domestic product lineup, which includes four ABCD models across the 60,000 to 300,000 yuan price range, overseas business has been a key growth driver.

Official data indicates that Leapmotor's overseas exports approached 100,000 units in the first half, already surpassing its total exports for all of 2025. Its pure electric models now command over a third of the market share in Italy, consistently topping local pure electric sales charts. On the day delivery figures were announced, Leapmotor Chairman Zhu Jiangming also disclosed the company's product roadmap: the first MPV model, D99, officially launched on June 25, the B-series will undergo a refresh in July, and a batch of innovative technologies will be unveiled in the third quarter to pave the way for new products. Clearly, Leapmotor aims to cement its current lead through continuous product and technological upgrades.

The race for second place is even more captivating. NIO delivered 40,597 units in June, up 62.88% year-over-year, marking a new single-month delivery high since 2026. With 191,123 units delivered in the first half, up 67.43% year-over-year, it also achieved its best-ever first-half performance. All three of its brands witnessed growth: NIO delivered 21,908 units, LEAPMOTOR delivered 11,743 units, and Firefly delivered 6,946 units. Its long-standing multi-brand strategy is finally paying dividends.

XPENG is closely trailing NIO, with a gap of less than 500 units. In June, XPENG delivered 40,126 units, up 15.93% year-over-year, returning to the 40,000-unit mark for the first time in seven months and achieving four consecutive months of month-over-month growth, signaling a clear recovery. Its new flagship model, GX, delivered 6,739 units in a single month. XPENG stated that with production line upgrades for core components, GX capacity will continue to ramp up, reducing the wait time for orders originally facing a 35-week delivery cycle by 1 to 3 weeks. On July 2, XPENG's first MONA series SUV, L03, made its China debut and opened for pre-sales, further expanding its growth potential.

Li Auto, in fourth place, had a lackluster performance. It delivered 30,895 new vehicles in June, down 14.84% year-over-year and month-over-month; its first-half deliveries totaled 193,472 units, down 5.13% year-over-year. Once a long-time leader among new forces, Li Auto now not only lags far behind Leapmotor but has also been surpassed by NIO and XPENG, dropping out of the top tier entirely.

Hidden Challenges Behind the Gloss

Despite the bright spots in each company's delivery data, a closer look reveals significant pressures for all.

Leapmotor, while surging ahead, carries the heaviest burden. Its annual sales target of one million units is only 35% complete in the first half, meaning monthly deliveries must exceed 107,000 units in the second half to meet the goal. Zhu Jiangming himself acknowledged that the target is highly challenging but not unattainable.

Now delivering 93,000 units in a single month, maintaining over 100,000 units consistently will test production capacity, channel coverage, and overseas market absorption. Moreover, the MPV segment is already fiercely competitive, and whether the D99 can replicate the success of other series remains to be seen.

XPENG's issues are concealed in its cumulative data. While four consecutive months of growth look impressive, its first-half deliveries totaled 165,977 units, still down 15.83% year-over-year. Simply put, last year's high base and this year's product transition period left a large gap that monthly recoveries have yet to fill.

Based on its annual sales target, XPENG is just over 30% complete in the first half, leaving significant pressure to ramp up in the second half. Whether GX capacity can be released as planned and whether the MONA series can gain traction in the entry-level market remain uncertain.

NIO's multi-brand layout appears robust across the board, but hidden concerns persist. The three brands target different segments, yet their price ranges inevitably overlap, raising questions about internal cannibalization and whether lower-end brands might dilute NIO's premium brand image. Additionally, with LEAPMOTOR and Firefly targeting affordable price points, their impact on overall gross margins remains unclear. While a 67.4% year-over-year growth rate in the first half is impressive, it only represents 40% completion of its annual target, requiring strong momentum in the second half.

Li Auto is in the most precarious position. The recent delivery decline is directly tied to a product iteration gap. The old L-series is nearing the end of its lifecycle, while the new L8 just launched on June 23 and the L6 won't arrive until July, creating a transition lull. Deeper issues include increased competition in the family SUV segment, where Li Auto's early advantages in extended-range technology and family positioning are being eroded by rivals. With its pure electric models lagging behind schedule and its extended-range base being siphoned off, Li Auto faces far more challenges than meet the eye.

Market Expansion Intensifies Competition

Viewing the new forces' performance within the broader auto market context, their fluctuations largely align with industry trends. Data from the China Passenger Car Association (CPCA) estimates June's new energy passenger vehicle retail sales at around 1.05 million units, up 10.5% month-over-month, with a penetration rate of approximately 63.6%—surpassing 60% for the third consecutive month.

CPCA Secretary-General Cui Dongshu noted that high fuel prices will continue to accelerate the electric vehicle transition. Coupled with end-of-half sales pushes, automakers are offering incentives like interest subsidies and purchase packages for new energy models, along with concentrated deliveries of new EV models, significantly boosting supply-side strength.

Driven by these favorable factors, the penetration rate of new energy passenger vehicles is expected to remain stable above 60%, with the electrification process accelerating. In other words, the new energy market is still expanding, and the pie is growing, allowing most brands to claim a share of the growth. However, the distribution of growth is uneven, with the leader effect intensifying. Brands like Leapmotor, which pursue full-stack self-research, high cost-performance, and overseas expansion, are capturing the most growth. NIO and XPENG are regaining their footing through product iterations and portfolio adjustments. Brands that hesitate or mishandle product transitions risk being left behind.

The second half of the year will only see fiercer competition. Leapmotor aims to hit one million annual sales, NIO must sustain multi-brand growth, XPENG hopes to break into the entry-level market with the MONA series, and Li Auto needs its new L-series to revive sales. With other cross-industry players continuing to enter the fray, the ranking battle among new forces is far from over.

The mid-year exam results bring joy to some and sorrow to others. But within China's new energy vehicle development trajectory, this is just one ordinary checkpoint in a prolonged competition. The true test lies not in single-month sales highs or lows, but in maintaining rhythm amid a rapidly changing market. Product, technology, channels, globalization—any weak link could lead to being overtaken by latecomers. The second-half whistle has blown; now it's time to see how each player responds.

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma