2025 Annual Dual Credit Report: Positive NEV Credits Exceed 21 Million Points

07/03 2026

07/03 2026

546

546

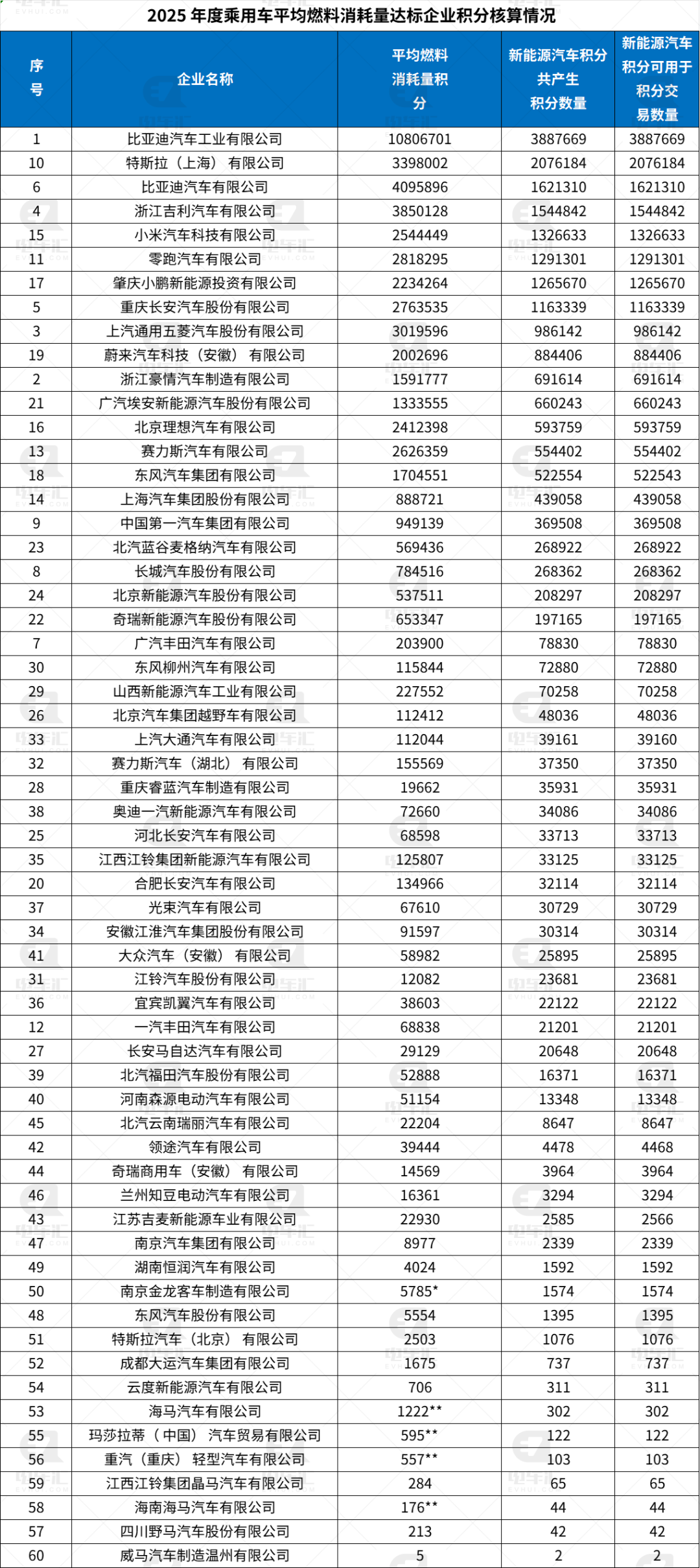

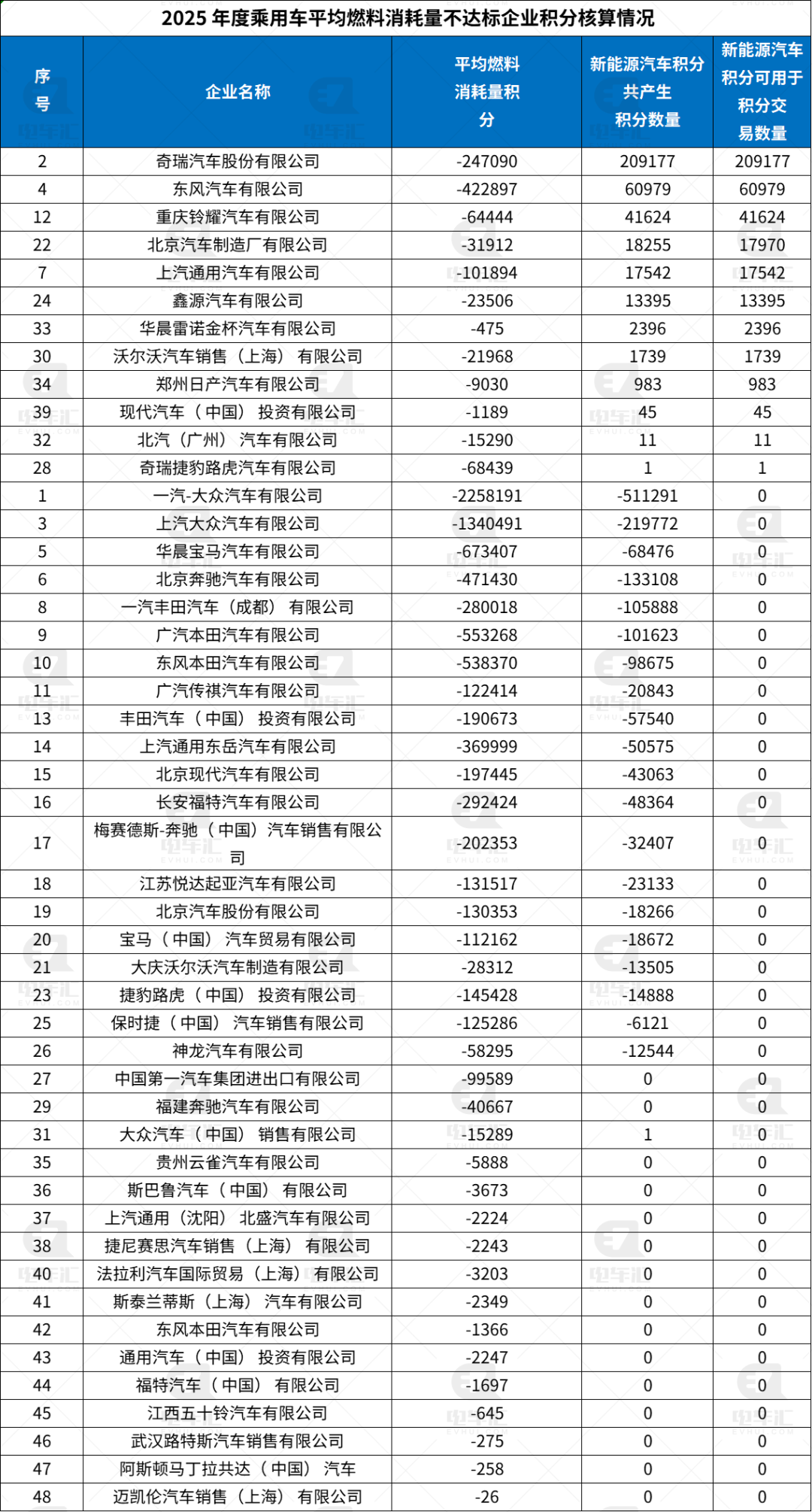

Recently, four departments, including the Ministry of Industry and Information Technology, officially released the 2025 annual report on the average fuel consumption and new energy vehicle (NEV) credits of China's passenger vehicle enterprises. This annual report not only offers a clear snapshot of the latest advancements in China's automotive industry concerning energy conservation, emission reduction, and NEV transformation but also unveils a significant transformation in the market landscape through detailed data analysis. According to the data, in 2025, 108 passenger vehicle enterprises in China produced or imported a total of 24.629 million passenger vehicles. The actual average fuel consumption of the industry stood at 3.38 liters/100 kilometers, with positive NEV credits reaching 21.940 million points and negative credits totaling 1.599 million points. Overall, the substantial surplus of positive NEV credits underscores the ongoing acceleration of the NEV transition in China's passenger vehicle market, while also highlighting a widening "wealth gap" among enterprises.

In terms of specific enterprise performance, NEV credit resources are increasingly concentrated among a select few leading companies, creating a distinct tiered structure. BYD, capitalizing on its deep-rooted expertise and scale advantages in the NEV sector, has emerged as the undisputed leader. The report reveals that BYD Auto Industry Co., Ltd. and BYD Auto Co., Ltd. collectively generated over 5.5 million NEV credits, with BYD Auto Industry Co., Ltd. alone producing nearly 3.89 million tradable credits, showcasing a commanding lead.

Trailing closely behind are Tesla (Shanghai) Co., Ltd. and Zhejiang Geely Automobile Co., Ltd., with tradable NEV credits of approximately 2.07 million and 1.54 million points, respectively, firmly securing their positions in the top tier. Additionally, emerging players such as Xiaomi Automobile Technology Co., Ltd., Leapmotor Co., Ltd., Chongqing Changan Automobile Co., Ltd., and Zhaoqing XPeng New Energy Investment Co., Ltd., along with traditional independent automakers, have also demonstrated robust performance, with tradable credits surpassing one million points, becoming key suppliers of credits in the market. Through technological innovation and strategic product positioning, these companies have not only achieved market sales success but also gained the upper hand in credit trading.

In stark contrast, some joint-venture automakers and luxury brands are grappling with significant compliance pressures under the dual credit assessment system. Among the list of compliant enterprises, although joint ventures like GAC Toyota and FAW Toyota managed to barely meet the requirements, their credit reserves are relatively weak. Conversely, traditional powerhouses such as FAW-Volkswagen, SAIC Volkswagen, BMW Brilliance, and Beijing Benz are prominently featured among non-compliant enterprises. Taking FAW-Volkswagen as an illustration, its average fuel consumption credit deficit exceeds 2.25 million points, and its NEV credits are negative, indicating that it cannot offset its fuel consumption negative credits through its own NEV models and must purchase substantial credits in the market to comply. Similarly, despite its massive total production, SAIC-GM-Wuling's fuel consumption negative credits have surpassed 300,000 points due to its product mix, underscoring the challenges of transformation. These figures suggest that joint-venture brands, once dominant in the Chinese market, will face escalating financial burdens and compliance risks if they fail to expedite their NEV sector initiatives.

Further data analysis reveals a stark divergence in the NEV transition performance between domestic and imported automakers. Among the 87 domestic passenger vehicle manufacturers, a cumulative total of 24.164 million passenger vehicles were produced, with an actual average fuel consumption of 3.30 liters/100 kilometers and positive NEV credits reaching a staggering 21.937 million points, while negative credits were only 1.469 million points. This data fully attests to the robust strength and first-mover advantage of domestic automakers in the NEV sector. In contrast, the 21 imported passenger vehicle suppliers imported 465,000 vehicles, with an actual average fuel consumption as high as 7.62 liters/100 kilometers and average CO2 emissions reaching 180.66 grams/kilometer. In terms of NEV credits, imported automakers only accumulated 3,000 positive NEV credits, while negative credits reached 130,000 points. The significant data disparity indicates that imported automakers have been relatively sluggish in responding to the NEV trend in the Chinese market and will confront even stricter compliance pressures and transformation challenges in the future.

With the continuous breakthroughs in NEV technologies, ongoing policy improvements, and heightened consumer environmental awareness, the NEV transition in China's passenger vehicle industry will further accelerate. The dual credit policy will continue to play its pivotal guiding role, steering the entire industry towards a more low-carbon and efficient trajectory. For companies holding a substantial number of positive credits, this is not only a badge of honor but also a tangible source of revenue; for those burdened with significant negative credits, this is no longer a distant warning but an immediate survival imperative.

-

![]()

Rokid's Ambition and Embarrassment: 300,000 Sales Can't Support Its Ecosystem Dream

-

Are Gaming Ventures No Longer in Vogue Among Tech Titans?

-

![]()

Kuaishou’s Keling AI, Valued at $18 Billion with a Five-Year IPO Pledge, Faces a Make-or-Break Challenge

-

![]()

Valued at $18 Billion with a Five-Year IPO Plan: Kuaishou’s Kling AI Takes a Bold Leap

-

![]()

NVIDIA Launches 'Computing Power Financing'

-

![]()

Following Up on the 'Safety Net' for Intelligent Driving: Is Huawei's Strategy Astute or Perilous?

-

![]()

ICML 2026 | One Model to Unify Humans, Objects, Sounds, and Actions: OmniShow Revolutionizes Multimodal Controllable Video Generation as a Systematic Engineering Feat!

-

![]()

Mid-Year Sales Analysis: Leapmotor Faces Challenges Alone, NIO Breaks Free from the 'NIO 30K' Stigma