Half-Year Pre-Tax Loss Hits 4.5 Billion, Full-Year Net Cash Outflow Reaches 16.2 Billion! GAC Incurs 8,000 Yuan Loss per Vehicle Sold

07/15 2026

07/15 2026

484

484

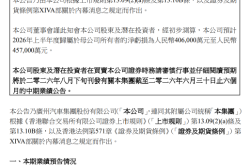

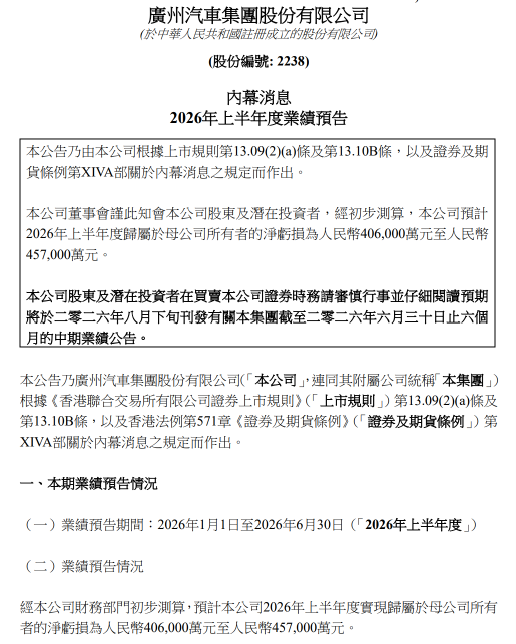

On July 10, GAC Group (601238.SH) issued a performance forecast, projecting a net loss attributable to the parent company's owners between 4.06 billion and 4.57 billion yuan for the first half of 2026. The net loss after excluding non-recurring gains and losses is estimated to range from 4.8 billion to 5.6 billion yuan. This represents a year-on-year increase in losses of approximately 60% to 80% compared to the 2.54 billion yuan net loss in the first half of 2025.

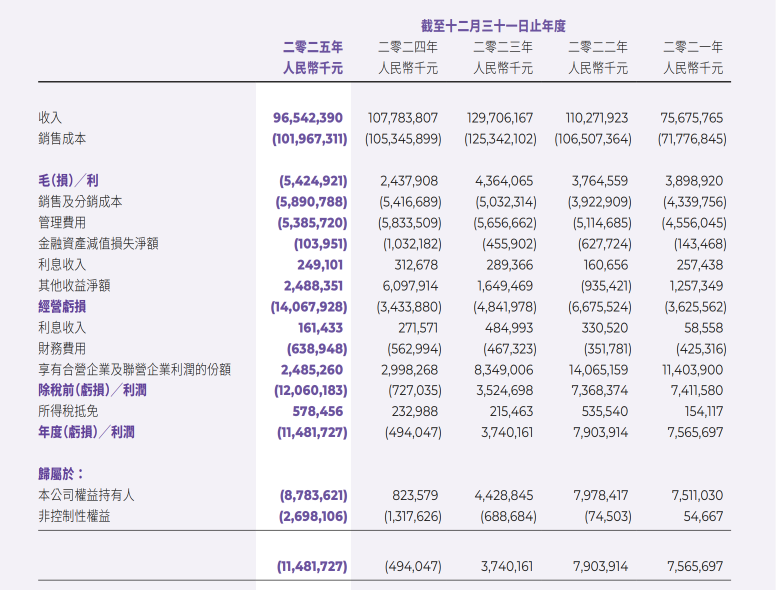

Source: GAC Group's H1 2026 Performance Report

[HK Stock Value Line] posits that the primary driver behind GAC Group's substantial losses is the escalating sales investment by its self-owned brands to navigate fierce market competition, compounded by diminishing revenue from joint venture brands.

Joint venture brands, once the linchpin of profitability, are now struggling. The investment income from GAC Honda and GAC Toyota plummeted from 8.349 billion yuan in 2023 to 2.485 billion yuan in 2025, marking a reduction exceeding 70%. Specifically, GAC Honda's sales in the first half of 2026 plummeted by 55.82% year-on-year, while GAC Toyota's monthly sales also turned negative.

Meanwhile, despite achieving sales growth, the company's self-owned brands, such as Aion and Trumpchi, which surged by 67.08% and 12.36%, respectively, are ensnared in a 'volume-for-price' predicament. Terminal discounts for key models range from 15,000 to 30,000 yuan, causing the gross profit per vehicle to shift from a 2,200 yuan profit per vehicle in 2024 to an 8,300 yuan loss per vehicle in 2025. Over three years, sales and distribution costs have surged by 17%, while revenue has declined by 26% during the same period.

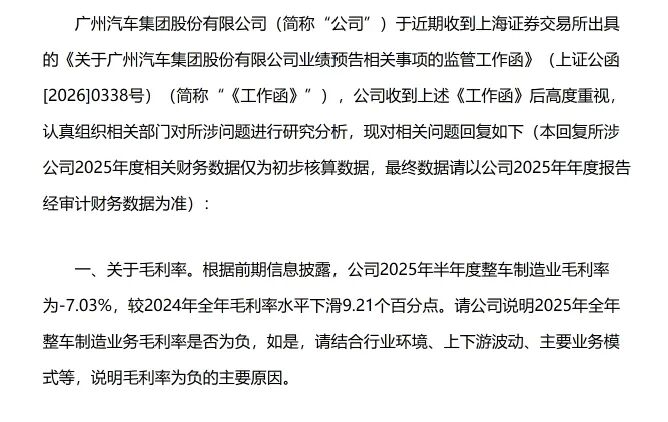

More alarming is the deterioration in the product mix. Sales of high-margin sedans and MPVs by GAC Group continue to decline, while sales of mid-to-low-end SUVs—the most fiercely price-competitive and least profitable segment—buck the trend with a 20% increase. The company's overall gross margin fell from 3.36% in 2023 to -5.62% in 2025, with the vehicle manufacturing business's gross margin as low as -7.35%.

From a regional market perspective, revenue in mainland China has plummeted by 43% over three years, shrinking by over 53.6 billion yuan. Although overseas revenue has more than doubled, the absolute increase is only about 11.5 billion yuan, far from sufficient to offset the domestic market shortfall.

Regarding cash flow, the company's operating cash flow has been negative for five consecutive quarters since 2025, with a net outflow of 16.199 billion yuan for the full year of 2025. Although it narrowed in the first quarter of 2026, the company remains in a precarious position, relying on existing funds to sustain operations, with severely impaired profitability in its core business.

01 Joint Venture Brands' Revenue Plummets, Self-Owned Brands' Heavy Sales Investment

GAC Group's losses are not an isolated phenomenon. In the first half of 2026, several automakers reported performance losses, with BAIC BluePark (600733.SH) losing between 1.77 billion and 1.97 billion yuan, Seres (601127.SH) losing between 1.5 billion and 1.8 billion yuan (shifting from profit to loss), and JAC Motors (600418.SH) losing approximately 740 million yuan. GAC Group ranks among the top in the industry with losses exceeding 4 billion yuan.

According to the announcement, the expansion of GAC Group's losses is primarily attributed to three factors: First, intensified domestic market competition and continuous increases in sales investment by self-owned brands, coupled with shifts in the product sales mix and rising upstream raw material costs, have led to an increase in losses for self-owned brands year-on-year.

Second, joint venture brands are facing operational pressures, with investment income decreasing year-on-year due to factors such as declining terminal sales, continuous increases in sales investment, and rising raw material costs.

Third, affected by exchange rate fluctuations, foreign exchange losses have occurred in the current period, further squeezing profit margins.

In simpler terms, self-owned brands have substantial sales investments, fierce market competition, and worsening losses, while joint venture brands are also experiencing declining sales.

Joint venture brands were once the most stable source of profits for GAC Group.

GAC Honda and GAC Toyota are the two main joint venture brands of GAC Group and also the company's core profit sources. The profit (i.e., investment income) contributed by these two companies to GAC Group, according to annual reports from 2023 to 2025, plummeted from a peak of 8.349 billion yuan in 2023 to 2.998 billion yuan in 2024 and further shrank to only 2.485 billion yuan in 2025.

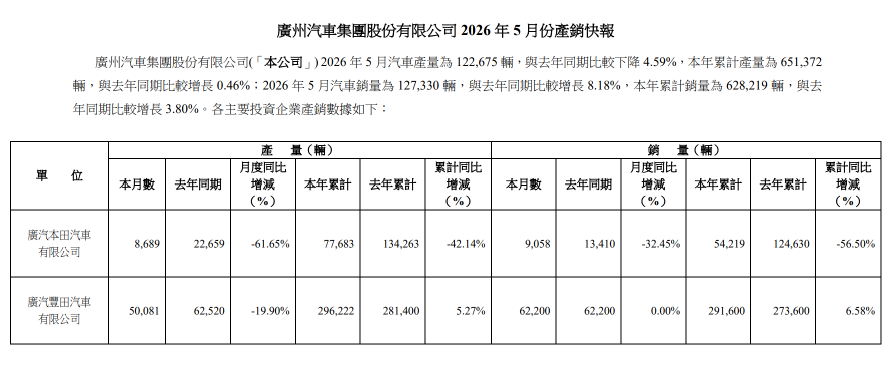

According to SAIC Motor's production and sales bulletin in June 2026, in the first half of 2026, GAC Honda's sales were only 68,300 vehicles, compared to 154,600 vehicles in the same period in 2025, a year-on-year plunge of 55.82%. GAC Toyota's sales in the first half of 2026 were 356,000 vehicles, compared to 344,700 vehicles in 2025, a slight increase of 3.29%, but monthly sales in June turned negative to -9.39% year-on-year.

In just three years, sales of GAC Group's two major joint venture brands have plummeted, and profits have shrunk by over 70%. The ability of joint venture brands to generate profits is diminishing.

GAC has lost its main profit barrier and is now focusing on self-owned brands.

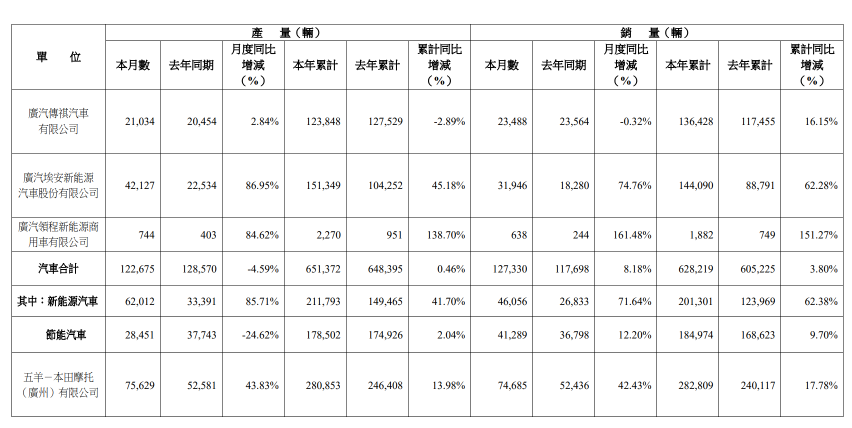

By brand, the two major self-owned brands show divergent performance. GAC Aion's sales reached 181,600 vehicles in the first half of 2026, surging by 67.08% year-on-year, while GAC Trumpchi's sales increased from 146,300 vehicles to 164,400 vehicles, a year-on-year increase of 12.36%.

However, the sales growth of self-owned brands has not led to profit improvement but has instead exacerbated losses due to increased sales investment.

GAC Group mentioned in its reply to the Shanghai Stock Exchange's regulatory letter that to cope with inventory pressure and the risk of declining market share, its main models of self-owned brands have increased promotional efforts, with terminal discounts generally ranging from 15,000 to 30,000 yuan, leading to a significant shrinkage in gross profit per vehicle.

Announcement data shows that in 2025, the revenue per vehicle of GAC's self-owned brands was 113,300 yuan, while the cost and taxes per vehicle were as high as 121,600 yuan, resulting in a gross loss of 8,300 yuan per vehicle sold, compared to a profit of 2,200 yuan per vehicle sold in the same period in 2024.

Data source: GAC Group's announcement

Data source: GAC Group's announcement

Reflected in the financial statements, the company's sales and distribution costs increased from 5.032 billion yuan in 2023 to 5.891 billion yuan in 2025, a 17% increase, while revenue decreased by 26% over the same period.

02 Decline in Sales of High-Margin Models, Tight Cash Flow

It is worth noting that GAC Group's overall revenue and net profit have already experienced significant declines.

According to GAC Group's 2025 annual report, the company's net profit attributable to owners of the parent company fell from 4.429 billion yuan in 2023 to 824 million yuan in 2024 and turned into a loss of 8.784 billion yuan in 2025. Revenue decreased by about 26% over three years, from 129.7 billion yuan to 96.5 billion yuan.

Operating losses expanded from 4.8 billion yuan in 2023 to 14 billion yuan in 2025, with losses in the main business also showing an expanding trend.

Data source: Futu Bull

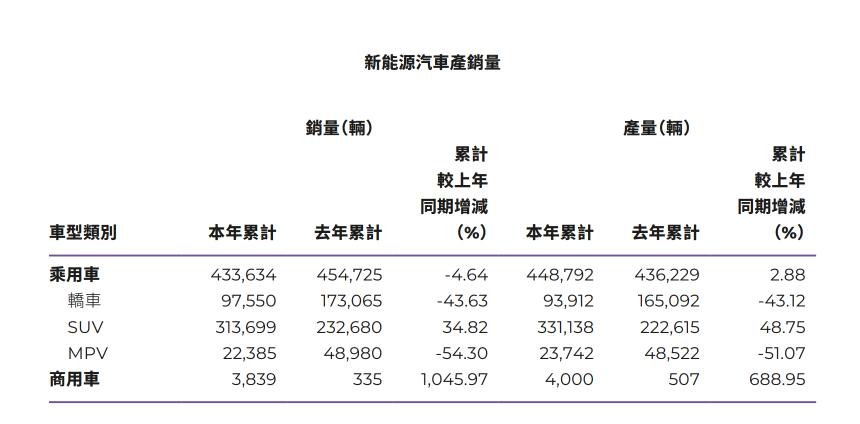

From a product mix perspective, sedan sales fell from 235,200 vehicles to 182,300 vehicles in the first half of 2025-2026, a decrease of -22.49%.

MPV sales fell from 112,500 vehicles to 99,800 vehicles, a decrease of -11.30%. SUV sales increased from 406,700 vehicles to 488,200 vehicles, an increase of 20.06%.

Image source: SAIC Motor's 2025 annual report

In GAC Group's product matrix, sedans (such as the Trumpchi GA series) and MPVs (such as the Trumpchi M8) are positioned in the mid-to-high-end segment and usually have higher profit margins.

The SUV market is the most fiercely price-competitive segment, especially mid-to-low-end SUVs in the 100,000-180,000 yuan range, where profit margins are severely compressed.

In the first half of 2026, the main drivers of SUV sales growth were mid-to-low-end models such as the Aion V and Trumpchi GS series.

The decline in sales of high-margin models and the increase in the proportion of low-margin models resulted in the company's overall gross margin falling from 3.36% in 2023 to -5.62% in 2025, with the gross margin of the vehicle manufacturing business only -7.35%. This is entirely consistent with the reason stated in the performance forecast that 'changes in the product sales mix' led to an expansion of losses.

Images sourced from SAIC Motor's production and sales bulletin in May 2025

In addition, the decline in revenue from the domestic market is more severe. By region, revenue from the mainland Chinese market was 124.185 billion yuan, 96.044 billion yuan, and 70.520 billion yuan in 2023-2025, respectively, plummeting by 43% over three years, with revenue accounting for 95.74% falling to 82.37%.

Meanwhile, revenue from overseas regions increased from 5.521 billion yuan in 2023 to 11.740 billion yuan in 2024 and further to 17.022 billion yuan in 2025, with the proportion jumping from 4.26% to 17.63%.

Although overseas revenue more than doubled over three years, the absolute increase was only about 11.5 billion yuan, while domestic revenue shrank by over 53.6 billion yuan, with overseas growth only filling about one-fifth of the domestic gap.

Furthermore, GAC Group's cash flow situation is also deteriorating. The company's net cash flow from operating activities has continued to experience large outflows, with -11.210 billion yuan in the first quarter of 2025, -11.461 billion yuan in the first half, -10.826 billion yuan in the first three quarters, and -16.199 billion yuan for the full year.

Image sourced from Futu Bull

Although it narrowed to -3.246 billion yuan in the first quarter of 2026, a significant improvement of 71.04% year-on-year, it has been negative for five consecutive reporting periods since 2025, indicating severely impaired profitability in the main business, with the company still relying on existing funds to maintain operations.

Source/HK Stock Value Line

-END -

-

![]()

Laying Off Hundreds of Thousands: Can European Automakers Triumph?

-

![]()

Seres: Navigating Beyond the 'Realm'

-

![]()

iFLYTEK Anticipates RMB 200 Million Loss, Embracing 'Subtraction' and 'Addition': Abandoning Low-Margin Businesses and Betting on AI's Future

-

![]()

ByteDance’s ‘Most Loyal’ U.S. Investor Exits, Notching 15,000-Fold Returns

-

![]()

DeepSeek’s Liang Wenfeng Becomes World’s Wealthiest in AI, Net Worth Skyrockets to $36 Billion

-

![]()

How Can Embodied AI Overcome the Data Challenge of 'Being Able to Work'? Solutions from Five Leading Players

-

![]()

Half-Year Pre-Tax Loss Hits 4.5 Billion, Full-Year Net Cash Outflow Reaches 16.2 Billion! GAC Incurs 8,000 Yuan Loss per Vehicle Sold

-

![]()

In a Bid to Propel Towards a $10 Billion IPO, Jieyue Xingchen Weaves a Hardware Fairy Tale: A 'Chinese Version of Apple + OpenAI'?