A 60% Plunge in Profits! Unraveling the Mystery Behind Great Wall Motors' Financial Setback

07/17 2026

07/17 2026

471

471

Recently, a semi-annual earnings forecast released by Great Wall Motors sent ripples through the capital market, causing quite a stir.

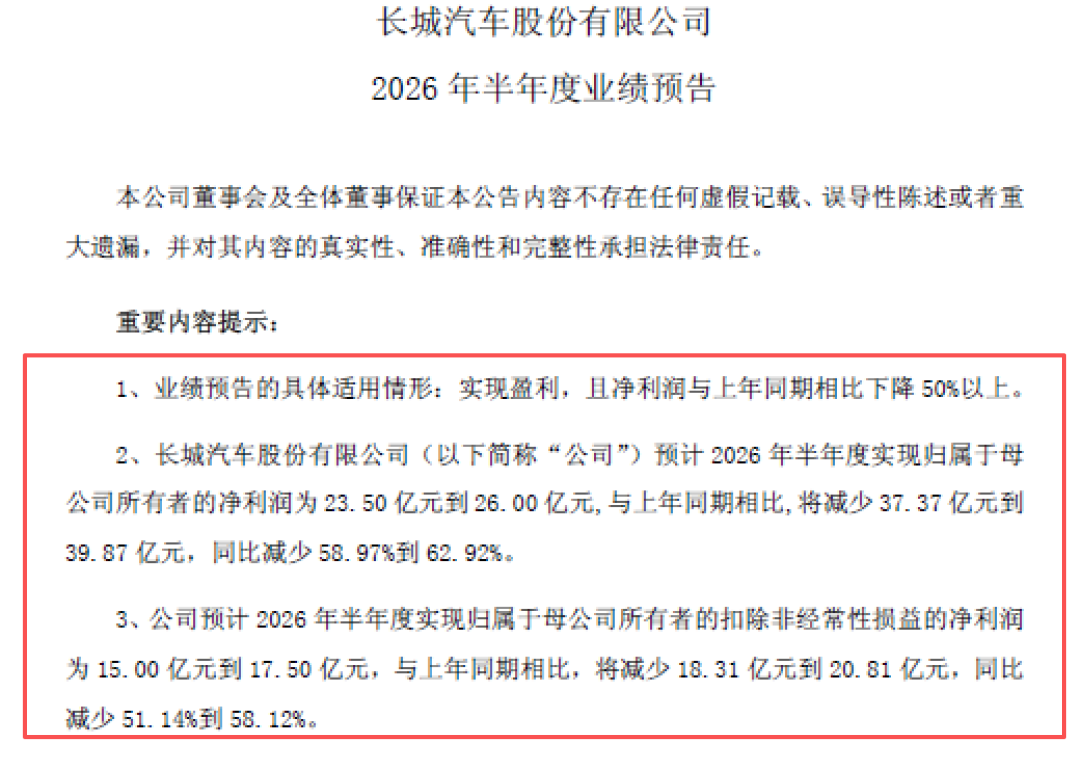

The net profit attributable to shareholders is projected to fall within the range of 2.35 billion to 2.6 billion yuan, marking a significant 59% to 63% year-on-year decline. Despite an uptick in both revenue and sales, profits have taken a nosedive, plummeting by 60%.

On the same day, Citigroup downgraded its rating from 'Buy' to 'Sell' and slashed its target price in half, further fueling market turmoil.

However, if we fixate solely on the figures presented in the report, we might overlook the most captivating aspect of this narrative.

Where Did the Profits Vanish?

Let's delve into the concrete data. In the first half of 2026, Great Wall Motors sold a cumulative total of 584,000 vehicles, representing a 2.5% year-on-year increase. Both revenue and sales also witnessed year-on-year growth. So, the question arises: where did the profits disappear?

Chairman Wei Jianjun's response was candid and to the point:

He cited two primary reasons: the delayed recovery of overseas tax subsidy benefits and adverse exchange rate fluctuations.

To put it bluntly, during the first half of the previous year, the company received 2.274 billion yuan in overseas scrap tax subsidies and 1.493 billion yuan in exchange gains. Together, these two items amounted to nearly 3.8 billion yuan, considered as 'unexpected windfalls.' This year, however, the subsidies were delayed, and exchange losses soared to 266 million yuan. The disparity between the two years exceeds 4 billion yuan.

According to Jefferies' research report, excluding these two factors, Great Wall Motors' core net profit for the first half of the year would hover around 6.4 billion to 6.6 billion yuan, roughly in line with the 6.34 billion yuan recorded during the same period last year.

In essence, Great Wall Motors' main business hasn't crumbled; rather, it's the 'non-recurring' items on the report that have taken a hit.

More notably, another set of data reveals that in the second quarter of 2026, the company's net profit attributable to shareholders is expected to range from 1.41 billion to 1.66 billion yuan, marking a 49% to 75% quarter-on-quarter increase. Operating profit also surged by 76% quarter-on-quarter.

What does this signify? It suggests that the darkest days may be behind us.

Sales Structure Undergoing a Qualitative Transformation

Now, let's shift our focus to the product layout. In 2025, Great Wall Motors' revenue reached 222.824 billion yuan, marking a 10.2% year-on-year increase; however, net profit attributable to shareholders declined by 22.07% year-on-year to 9.865 billion yuan. Sales reached 1.3238 million vehicles, representing a 7.23% year-on-year increase. Among them, new energy vehicles accounted for 406,000 units, marking a 26% year-on-year increase; overseas sales reached 506,800 units, an 11.6% year-on-year increase.

In 2026, structural changes have become even more pronounced.

Exports in the first half of the year reached 291,000 units, marking a 47.4% year-on-year increase. In June, exports accounted for over 55% of total sales. In May, exports exceeded 50% for the first time. Overseas markets now constitute half of the business.

The brand structure is also evolving. WEY brand sales reached 45,000 units in the first half of the year, marking a 29.1% year-on-year increase. ORA brand sales reached 26,000 units, an astonishing 89.7% year-on-year increase. Although Haval and Tank sales declined, high-end and new energy brands are experiencing rapid growth.

Data Sources: Great Wall Motors' 2025 Annual Report, 2026 Semi-Annual Earnings Forecast, 2026 June Production and Sales Report

Industry Shakeout: Who's Exposed and Who's Protected?

Placing Great Wall Motors within the broader industry context sheds further light on the situation.

In the first half of 2026, China's passenger vehicle retail sales reached approximately 8.75 million units, marking a roughly 20% year-on-year decline. However, new energy vehicle penetration surpassed 60% from April onwards, maintaining historic highs for three consecutive months. In June, it reached 63.6%. Sales of fuel-powered vehicles plummeted, while new energy vehicles surged ahead.

The entire market is undergoing a structural, irreversible transformation.

Against this backdrop, Great Wall Motors' new energy vehicle share stands at around 30%, lagging behind the industry average. Its domestic sales in June reached only 47,900 units, being overtaken by new forces like Leapmotor and HiMo. This is a fact that cannot be ignored.

However, from another perspective: In 2026, when the fuel-powered vehicle market is rapidly shrinking and industry-wide price wars intensify, Great Wall Motors still achieved double-digit growth in sales and revenue, with overseas markets maintaining over 47% growth. This is not the story of a 'loser.'

Wei Jianjun made a remark worthy of contemplation: 'While surface numbers are important, we care more about the healthy development of the enterprise.' He also revealed that the company 'sells more but issues fewer vehicles, with domestic inventory-to-sales ratios better than the industry average.'

While peers are desperately pushing inventory to boost sales, Great Wall Motors has chosen to control the pace. In the short term, this sacrifices report numbers, but in the long term, it protects the channel ecosystem.

An Underestimated Trump Card

In 2025, Great Wall Motors unveiled the world's first native AI all-powertrain automotive platform—the Guiyuan Platform—compatible with multiple power forms and seven major vehicle categories. The first model, WEY V9X, was launched in May 2026. New mid-to-high-end models like the all-new Tank 300 and Great Wall H10 based on this platform will be launched in the second half of the year.

The significance of the platform strategy extends beyond cost reduction and efficiency gains. It signifies that Great Wall Motors has finally transitioned from 'multiple brands operating independently' to 'unified technological platform empowerment.'

After the launch of WEY V9X, equipped with the Super Hi4 plug-in hybrid system, 6C ultra-fast charging, and a CLTC combined range of up to 1,700 km, the Menglong PLUS received over 20,000 orders within 24 hours of its launch. These are not 'outdated' products.

In 2026, Great Wall Motors aims to sell 1.8 million vehicles. With 584,000 units sold in the first half of the year, the completion rate stands at 32%. The pressure in the second half is significant. However, considering the flurry of new model launches, sustained export growth, and significant Q2 profit improvements, this target is not out of reach.

Long-Termism Is Never Just a Slogan

This 'earnings turmoil' actually serves as a wake-up call for the entire automotive industry.

Firstly, reported profits can be deceptive; operational quality cannot. Great Wall Motors' profits plummeted by 60% in the first half of the year, but its core operating profit remained flat year-on-year. Judging a company's 'death sentence' based solely on net profit misreads its true value.

Secondly, going overseas is a necessity, not a choice. When domestic competition intensifies and price wars become endless, overseas markets provide a second growth engine. Great Wall Motors' export share reached 50% in the first half of the year, indicating it's on the right track.

Thirdly, price wars won't secure the future; technological competition will. In 2026, China's auto market has witnessed price wars from the beginning to the middle of the year, putting continuous pressure on industry profitability. Great Wall Motors has chosen 'value competition' over 'low-quality price wars.' While this may result in some market share loss in the short term, it safeguards the brand's bottom line in the long run.

Great Wall Motors is 36 years old. Throughout China's automotive industry's journey from stumbling steps to global expansion, it has been a participant and contributor. In my view, this earnings fluctuation is more like 'growing pains' during a transformation period rather than a 'terminal illness.'

When the tide recedes, we see who's exposed.

And the one who remains protected, adjusts their breathing, and prepares to dive deeper deserves our patience.

Go, Great Wall Motors! Go, Old Wei!

What's your take on this topic?

-

![]()

Autonomous Driving Enters the Second Half: ByteDance Enters the Field, NVIDIA Restructures, and the First IPO Emerges

-

![]()

Service Takes Center Stage: A 2026 Mid-Year Analysis of BBA Reputation Index

-

![]()

The Paradox of Car Sales: Why Do Automakers Keep Launching New Models Amid Rising Losses?

-

![]()

"If We Can't Find a Breakthrough in Three Years, We're Finished": Japanese Cars Are Increasingly Emulating Chinese Models

-

![]()

After Missing Independent Listing, Will Zhang Di Forge a Kling-like Success at Alibaba?

-

![]()

1100 Enterprises, Over 300 Worldwide Debuts! Six Key Highlights of the 2026 World Artificial Intelligence Conference

-

![]()

Xiaopeng IRON to Reach 1,000-Unit Monthly Production by Year-End: Humanoid Robots Set to Revolutionize Car Sales Before Factory Work?

-

![]()

Volkswagen's Crisis Began with a Decision in China 20 Years Ago