Facing the Worst Interim Report in 7 Years: Changan Bids Farewell to Scale-Centric Approach, Emphasizing Product Profitability | Mirror Pro

07/17 2026

07/17 2026

574

574

"Changan is no longer solely focused on scale; products must be profitable. Changan has established an internal operational co-investment mechanism where projects will fail if products do not generate profits, even if sales targets are met," media reports quoted Tan Benhong, Deputy Secretary of the Party Committee and Director of China Changan Automobile Group Co., Ltd., as saying at Changan Automobile's mid-year media briefing on July 16. "Merely pursuing volume to outcompete others through scale is a strategy Changan will use cautiously. Balancing volume and profit is crucial."

It can be said that at the mid-year briefing, Changan's senior leadership signaled a stronger strategic shift away from a 'scale-centric' approach, price wars, and toward higher-quality, more sustainable profits than at the beginning of the year.

Changan is proactively making 'subtractions' to enhance profit quality. According to reports, Tan Benhong stated at the briefing that Changan voluntarily discontinued some high-volume but low-margin products in the first half of the year, with the Changan Nuomi being a representative example. "The Nuomi, priced under RMB 50,000, was adjusted proactively. We sold 70,000 units of this product in the first half of the year alone, but we cut products with low profitability. Of course, you can have scale, but we are constantly re-evaluating such products and have decided not to pursue them," Tan said.

Data shows that Changan Nuomi's monthly sales remained at 10,000-20,000 units in 2025, dropping below 10,000 units in December last year. Since the beginning of this year, its sales have largely stayed between 1,000-2,000 units. This decline is attributed to both Changan's proactive contraction and the overall market downturn. For instance, the market leader, Wuling Hongguang MINI EV, saw its monthly sales drop from 50,000-60,000 units to 20,000-30,000 units, roughly halving. Achieving profitability with such A00-class microcars is understandably challenging.

This strategy of streamlining product lines was a predetermined policy (policy) for Changan this year. On April 21, during the Global Strategy Release and Global Partners Conference hosted by China Changan Automobile Group, Zhu Huarong, Chairman of Changan Automobile, stated that over the next five years, the company would further focus on major products, reducing its product portfolio from 63 models to 36, a 43% reduction. It aims to create one global bestseller with annual sales of 500,000 units and five with annual sales of 300,000 units. By 2030, Changan targets annual production and sales of 4 million vehicles, striving for 5 million, with Avatr contributing 500,000 units, Deepal 1 million, and the Changan brand 2.6 million. New energy vehicles will account for over 60%, with overseas sales making up 35%-40%.

Additionally, differentiated market strategies and upward price band shifts are being implemented. Yang Dayong, Executive Vice President of Changan Automobile Co., Ltd., reportedly stated at the conference that while the LUMIN model contributed around 200,000 units in sales last year, this volume is being proactively reduced this year due to multiple policy factors. Instead, the Qiduan Q05 is taking its place. Data shows that this compact SUV sold 19,350 units in May and 23,523 units in June, with cumulative first-half sales exceeding 76,000 units. It has consistently ranked among the top sellers in the highly competitive compact SUV segment, dominated by fuel vehicles, becoming a new sales pillar. This marks Changan's initial success in transitioning its mainstay products.

Tan Benhong emphasized the importance of differentiated competition in the future, noting that homogenization leads to price wars, resulting in cheaper products and a narrower product range—a logic detrimental to industry development. Yang Dayong also hinted that the latest model, Changan Qiduan Q06, would not adopt a low-price strategy. He pointed out that while the company continues to pursue cost reductions and efficiency improvements internally, significant price hikes in core components like battery raw materials and chips have offset these efforts, yielding limited actual results. Therefore, the Changan Qiduan Q06 must shoulder the responsibility of profitability.

Changan's strategic choice is understandable. Judging from its 2025 financial report and 2026 interim report, Changan's profits are disproportionate to its scale.

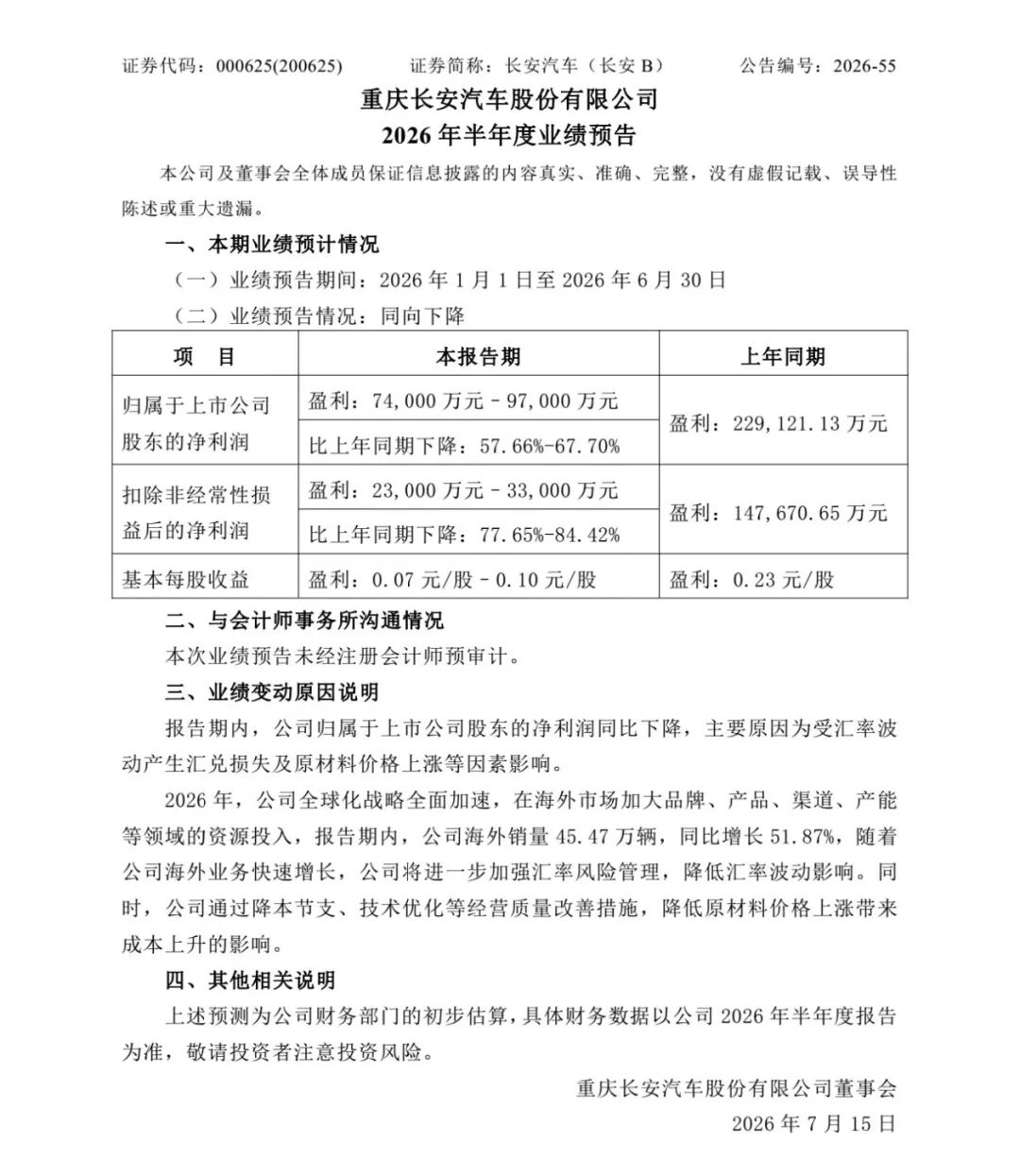

On the evening of July 14, Changan Automobile announced that its net profit attributable to shareholders for the first half of the year is expected to be RMB 740 million to RMB 970 million, a year-on-year decline of 57.66% to 67.70%. Net profit for the same period last year was RMB 2.291 billion, representing a roughly two-thirds decrease this year. This performance marks Changan's worst interim report since 2019. Historically, only in 2019 did Changan report a loss of RMB 2.24 billion in its interim report; subsequently, its interim profits have generally hovered around RMB 2 billion.

However, in terms of sales volume, Changan Automobile delivered a cumulative 1.1956 million vehicles in the first half of the year, a 17.44% year-on-year decline, though still at a historically high level overall. Within this sales structure, new energy vehicles accounted for 456,000 units, a 5.2% increase, while overseas sales reached 402,000 units, a 35.1% increase. This indicates that the year-on-year decline in Changan's net profit attributable to shareholders far exceeds changes in sales volume, suggesting relatively weak profitability.

From the perspective of independent brand sales, among the top five independent brands, Changan's target completion rate for the year stands at 36.23%. To achieve its annual sales target of 3.3 million units, it must sell 2.105 million vehicles in the remaining six months, averaging 350,000 units per month. For Changan, reaching monthly sales of over 300,000 units in the current market environment indeed poses a significant challenge.

Secondly, from a capital market perspective, as of July 7, Changan Automobile's stock price had declined by 40.39% (Wind data). Among top automakers, Changan is one of the two with the highest declines. Great Wall Motor (Hong Kong stock down 40.97%, A-share down 31.46%), Chery Automobile (Hong Kong stock down 16.29%), BYD (A-share down 11.73%), and Geely Automobile (Hong Kong stock up 10.16%). From a performance standpoint, Changan Automobile's first-quarter report for 2026 showed revenue of RMB 32.7 billion, a 4.26% year-on-year decline. Affected by exchange rate gains and losses, net profit attributable to shareholders was RMB 350 million, a 74.09% year-on-year decline. This profit scale and decline rank it last among the five automakers.

In 2025, Changan achieved revenue of RMB 164 billion, a 2.67% year-on-year increase. Net profit attributable to shareholders was RMB 4.075 billion, a 44.34% year-on-year decline from RMB 7.321 billion in the previous year. Therefore, enhancing operational quality has become an inevitable trend for Changan. Especially during a period when the entire industry is embroiled in price wars and unnecessary competition, Changan, as a new central enterprise, must pioneer a more sustainable and higher-quality development path.

Regarding new energy brands, Changan has also formulated its profit plans. In a recent Q&A session with investors, Changan stated that to accelerate the development of its three major new energy brands and achieve profitability for Qiduan and Deepal, as well as significantly reduce losses for Avatr. From this statement, it is evident that Changan's goal is to first achieve profitability for Qiduan and Deepal before driving Avatr towards profitability.

Additionally, Changan responded to inquiries about the integration progress of Deepal and Avatr. Tan Benhong stated that Avatr and Deepal are pursuing differentiated development but will share platform architectures, three-electric systems, intelligent driving software stacks, and supply chain procurement. Deepal's high-end models will reuse Avatr's 896-line LiDAR, while Avatr can leverage Deepal's large-scale procurement to reduce BOM costs. Through technology sharing and centralized procurement, cost reductions of 20% to 30% are expected, thereby halting losses.

Simultaneously, Changan is also moving away from a sales-centric approach in its premium brand development. Tan Benhong noted that while Avatr's sales fluctuated in the first half of the year, its premium positioning remains intact. For instance, Avatr's average selling price this year has significantly increased compared to last year. Moreover, its gross margin rose to 9.4% in 2025, indicating continued pricing power for premium products. Secondly, Changan's understanding of 'premiumization' is evolving. Premium brands require service, branding, and more resources, rather than simply selling vehicles. Avatr is already facing this challenge, as significant resources must be allocated to services post-sale.

In other words, Changan has chosen not to blindly pursue sales volume in the premium segment. However, for Avatr, which is in the process of going public, convincing investors poses a challenge.

"Automobiles are a marathon. And it's a marathon without a finish line," Tan Benhong said. Besides strategic adjustments this year, Changan is also making significant strides in HEV technology. In May, Changan officially launched the Blue Whale Super Engine HEV hybrid system, bringing mainstream HEV hybrids into the RMB 70,000 price range. Starting in August, hybrid versions of the CS55 and UNI-V will be sequentially launched. Yang Dayong, Executive Vice President of Changan, revealed that while current HEV monthly sales are limited to around 5,000 units due to battery supply constraints, "starting in August, with four hybrid models in full swing, selling 15,000 units per month should not be a problem."

This indicates that HEVs will become a new growth point for Changan, serving as a testament to its refusal to engage in internal competition and its commitment to high-quality development.

-

![]()

Autonomous Driving Enters the Second Half: ByteDance Enters the Field, NVIDIA Restructures, and the First IPO Emerges

-

![]()

Service Takes Center Stage: A 2026 Mid-Year Analysis of BBA Reputation Index

-

![]()

The Paradox of Car Sales: Why Do Automakers Keep Launching New Models Amid Rising Losses?

-

![]()

"If We Can't Find a Breakthrough in Three Years, We're Finished": Japanese Cars Are Increasingly Emulating Chinese Models

-

![]()

After Missing Independent Listing, Will Zhang Di Forge a Kling-like Success at Alibaba?

-

![]()

1100 Enterprises, Over 300 Worldwide Debuts! Six Key Highlights of the 2026 World Artificial Intelligence Conference

-

![]()

Xiaopeng IRON to Reach 1,000-Unit Monthly Production by Year-End: Humanoid Robots Set to Revolutionize Car Sales Before Factory Work?

-

![]()

Volkswagen's Crisis Began with a Decision in China 20 Years Ago